Record half for Retail lending and customer transactions

Record half for Retail lending and customer transactions

Dubai, 28 July 2022

Emirates NBD delivered its highest first-half profit since 2019. Q2 profit was exceptionally strong at AED 3.5 billion, up 42% y-o-y. Another record half-year for retail lending and customer transactions together with improving margins drove income up 23% y-o-y. Credit quality across the Group's footprint continues to improve with impairment down 28%. These results build on the economic recovery momentum from 2021. With its strong profitability and balance sheet the Group's short and long-term Moody's ratings have been upgraded. We are extremely well positioned for rising interest rates and will continue to invest in our international and digital capabilities to support further growth. Emirates NBD is proud to have played a leading role in the DEWA and TECOM IPOs, delivering customers a fully digital platform from on-boarding and subscription through to payment.

Key Highlights – First Half 2022

- Increase in operating performance as loan and deposit mix improved on continued record demand for retail financing, an efficient funding base and a substantially lower cost of risk

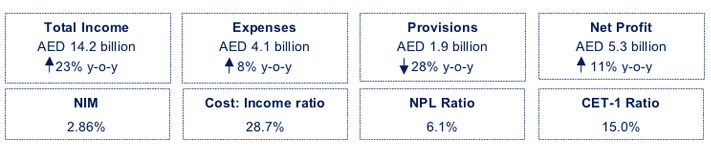

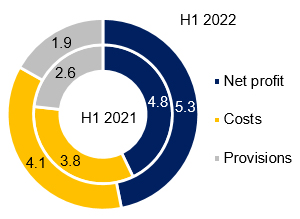

- Total income up 23% y-o-y to AED 14.2 billion on improved loan mix and cheaper deposits with higher interest rates feeding through to margins

- Net interest margin guidance raised by 50bps due to higher interest rates and improving margins in DenizBank

- Expenses well controlled, with high income enabling the Group to accelerate investment in Advanced Analytics and international network to drive future growth

- Impairment allowances substantially down 28% y-o-y reflecting strong writebacks and recoveries and an improving economic outlook

- Net profit of AED 5.3 billion up by a healthy 11% y-o-y

- Earnings per share up 14% to 80 fils for H1-22, underlying up 57%

- Emirates NBD's strength empowers its customers to benefit from a growing economy

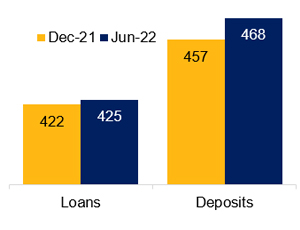

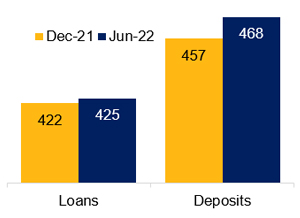

- Total assets: up 3% at AED 711 billion

- Customer loans: up 1% at AED 425 billion with a record half-year for retail financing and renewed demand for corporate lending.

- Deposit mix: CASA grew AED 10 billion in H1-22 reflecting strong UAE liquidity, enabling the Group to benefit from further interest rates rises

- Credit quality: NPL ratio improved by 0.3% to 6.1% in Q2-22 on healthy writebacks and recoveries as the economy continues to strengthen. Coverage ratio very strong at 133.3%

- Capital and Liquidity: 155% Liquidity Coverage Ratio and 15.0% Common Equity Tier-1 ratio reflect the Group’s solid balance sheet, used to empower customers and create opportunities to prosper

- Emirates NBD's digital transformation enables agile delivery of new services and increased straight through processing

- Moody’s upgrade Emirates NBD’s short and long-term ratings recognising the Group’s resilient post-pandemic financial fundamentals and increased diversification.

- 30% market share: Emirates NBD and Emirates Islamic have close to a combined 30% market share of UAE Debit and Credit Card spend.

- International revenue diversifies income, representing 41% of total revenue

- IPO: leading role in the DEWA and TECOM IPOs, delivering customers a fully digital platform enabling a seamless, paperless journey from on-boarding and subscription through to payment

- Digital: 93% of new product and servicing requests now fully automated, with 5% y-o-y improvement eliminating 4 million manual interventions annually

- ESG: proudly support the ‘Dubai Can sustainability initiative’, Emirates NBD sponsor a public water refill station, which has saved 91,000 single-use plastic bottles since February 2022

- Talent: launched the ‘National Digital Talent Program’ giving a UAE talent pool practical knowledge in Digital, IT and Artificial Intelligence, supporting the UAE Government’s National Strategy for Artificial Intelligence 2031

Hesham Abdulla Al Qassim, Vice Chairman and Managing Director said:

- “Emirates NBD’s profits jumped 42% y-o-y to AED 3.5 billion in Q2-22, reflecting the strong regional economy and the Group’s diversified sources of income.

- Emirates NBD played a leading role in both the DEWA and TECOM IPOs, delivering customers a fully digital, straight through platform from on-boarding to payment.

- We were delighted that Moody’s upgraded Emirates NBD’s short and long-term ratings, recognising the Group’s resilient post-pandemic financial fundamentals and increased diversification.

- Emirates NBD has doubled down on its commitment to develop Emirati talent. In addition to enhancing the Bank’s mainstream graduate program, which attracts over 100 graduates per year, we launched the ‘National Digital Talent Program’ giving a UAE talent pool practical knowledge in Digital, IT and Artificial Intelligence, supporting the UAE Government’s National Strategy for Artificial Intelligence 2031.”

Shayne Nelson, Group Chief Executive Officer said:

- Emirates NBD delivered strong results with total income rising 23% to AED 14.2 billion on improved loan and deposit mix, with higher interest rates feeding through to margins.

- International operations contributed 41% of total income in H1-22.

- New lending increased substantially with a record half-year for retail lending and renewed corporate lending demand.

- Impairment allowances substantially down 28% y-o-y reflecting the improving operating environment

- 93% of new product or servicing requests are now fully automated, with a 5% improvement on last year eliminating 4 million manual interventions annually.

- These strong results, along with the positive outlook for margins, enable us to accelerate our investment in our international network and digital capabilities, supporting our next stage of growth.”

Patrick Sullivan, Group Chief Financial Officer said:

- “We have maintained good income growth momentum, kept a firm control of costs and seen a consistent decline in the cost of risk.

- Net profit of AED 5.3 billion increased by a healthy 11% y-o-y, comfortably absorbing the impact from inflation in Turkey.

- The UAE banking sector continues to benefit from ample liquidity, helped by the high oil price. In H1-22 we grew CASA balances by AED 10 billion, enabling the Group to benefit from interest rates rises.

- In light of further expected rate rises, coupled with improving margins at DenizBank, we have raised our net interest margin guidance raised by 50bps.

- Non-funded income also grew, with significant contributions from both Emirates NBD and DenizBank, helped by an increase in transaction volumes and growth in customer foreign exchange and derivative business.

- The diversified balance sheet, solid capital base and strong operating profitability are core strengths of the Group.”

Financial Review

Operating Performance

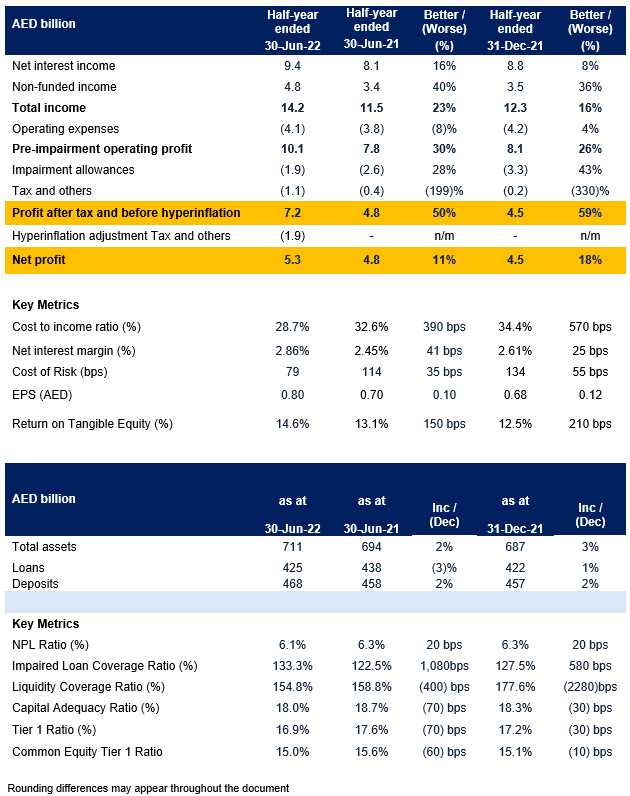

Total income for H1-22 was up 23% y-o-y to AED 14.2 billion. Net interest income was up 16% y-o-y on improved loan and deposit mix with higher rates feeding through to margins. Further CASA growth improved funding costs and the balance sheet is well positioned to continue benefiting from rate rises. Non-funded income was up 40% y-o-y from increased local and international card transactions, coupled with growth in FX & Derivative income.

Expenses remain well controlled and within guidance. Higher income from rate rises enables accelerated investment in Advanced Analytics and the international network to drive future growth.

Impairment allowances in H1-22 were down substantially 28% y-o-y reflecting higher recoveries and writebacks and the improving operating environment, with 79 bps cost of risk lower than guidance.

Balance Sheet Trends

Loan increased by 1% in H1-22, with a strong half-year for EI and Retail financing which grew by 11% and 8% respectively with DenizBank's loans up 26%.

Deposit mix improved in H1-22 with AED 10 billion growth in CASA enabling the Group to benefit further from interest rate rises.

Liquidity remains strong with the Liquidity Coverage Ratio at 154.8% and the Advances to Deposits Ratio at 90.8%.

During the first half of 2022, the Non-Performing Loan ratio improved by 0.2% to 6.1% whilst the Coverage ratio strengthened to 133.3%, demonstrating the Group's continued prudent approach towards credit risk management.

As at 30 June 2022, the Group's Common Equity Tier 1 ratio is 15.0%, Tier 1 ratio is 16.9% and Capital Adequacy ratio is 18.0%.

Business Performance

- Retail Banking and Wealth Management (RBWM) had an excellent first half with highest ever revenue, strongest ever acquisition of loans and credit cards, and a record growth in balance sheet.

- Robust business momentum continued in the UAE with H1 Loan origination up 41% y-o-y, Credit Card acquisitions up 100% y-o-y and Card spends up 35% y-o-y

- Customer advances increased by AED 4.9 billion, whilst CASA grew by a record AED 15.5 billion in H1

- Income up 17% y-o-y with RBWM delivering its highest ever half yearly revenue and fee income

- Emirates NBD Etihad Guest Credit Card launched, offering one of the highest Etihad Guest earning and rewards opportunities and signed a 5-year strategic partnership with RSA covering general insurance products

- Launched DEWA and TECOM IPO portal on Emirates NBD website with real time direct integration with DFM

- Corporate and Institutional Banking (C&IB) developing strategic partnership with major Government entities and Corporates by digitizing service platforms.

- Took lead in supporting IPOs, with end-to-end IPO subscription website offering real-time on-boarding through a state-of-the-art fully digital platform

- Implemented cutting-edge new platform for businessONLINE

- Net Profit jumped 10% y-o-y on higher fee income and lower impairment allowances

- Strong growth in new lending offset substantial contractual repayments

- Global Markets and Treasury (GM&T) delivered a strong performance with net interest income growing 264% y-o-y in H1-22 due to higher income from balance sheet positioning, hedges and an increase in banking book investment income.

- Non funded income was 289% higher with a significant performance delivered by Rates, Credit and Foreign exchange Trading.

- International Treasury functions made a significant contribution, growing their revenue contribution by 186%.

- Emirates Islamic's net profit up 23% y-o-y to AED 701 million on higher income and lower impairment allowances and customer financing grew 11% in H1-22.

- DenizBank income up by AED 1.4 billion (42%) and Impairment allowances AED 0.6 billion lower on strong writebacks and recoveries helping offset AED 1.9 billion hyperinflation adjustment.

Outlook

For the UAE and the GCC, higher oil prices will push budgets into surplus and reduce the need for sovereign debt issuance this year. Central Bank statistics show that the UAE's economy expanded by 8.2% y-o-y in the first quarter of 2022, led by higher oil production and strong 6% growth from the non-oil sector, as the country benefitted from increased travel & tourism, coupled with the positive impact of Expo 2020.

Global Inflation at multi-decade highs has led to interest rates rising at a faster pace than had been expected just a few months ago. The Federal Reserve is expected to raise rates by at least another 200bp before year-end.

Egypt and Turkey have seen a strong surge in services inflow and tourism revenue as global travel resumed, which is offsetting some of the impact from rising energy costs on the current account deficit.

UAE

UAE